ARM Vaults Thrive During Volatility

Origin’s ARM is a liquidity venue built around a single premise: redeemable assets have two prices. The market price, where they trade on DEXs, and the redemption price, where they settle 1:1 through the underlying protocol.

In stable market conditions, those two prices stay close. The arbitrage opportunity is narrow and ARM Vault yield converges toward lending rates. In volatile markets, the gap widens substantially.

Increased market volatility means more yield returned to ARM LPs. This is the core concept of the ARM’s design.

The ARM Operates in Two States: Active Arbitrage and Lending.

At any given moment, capital in an ARM Vault is in one of two states.

When no qualifying arbitrage opportunity is present, idle capital routes to a lending market. For the stETH and eETH ARMs, capital is routed to Morpho. For the sUSDe ARM, deposits route to Aave V3. The lending rate sets the yield floor: the ARM will not execute arbitrage unless the opportunity clears this threshold.

When a redeemable asset trades at a qualifying discount on the secondary market, the stETH and eETH ARMs allow users to swap LSTs for ETH, and the ARM receives LSTs at a discount. It initiates the underlying protocol's redemption process, and receives the base asset at 1:1 when the redemption settles.

The spread is returned to LPs: the difference between the discounted purchase price and the 1:1 redemption value translates to yield generated by the ARM Vaults.

ARM Bids Are Priced Against Redemption Time and Discount Size

The ARM does not sell assets for every discount it finds. It sells when the implied yield crosses the yield threshold: the annualized return implied by the discount must exceed what the same capital would earn in the lending market over the expected redemption period.

That period is determined by the protocol’s withdrawal queue. For the stETH ARM, Lido's queue sets the redemption window. When queues are short, the ARM sells ETH for stETH at as small as 1-2 basis points discounts, provided the annualized yield clears Morpho lending rates. When queues lengthen, the minimum qualifying discount rises: larger discounts are required to justify longer capital lockup.

This creates a counterintuitive dynamic under market stress. Queues lengthen during volatility, and a longer queue means the ARM must bid lower to clear its yield threshold. But secondary market discounts widen faster than queues lengthen. The ARM bids lower, and the bids still fill at spreads that produce substantially higher annualized yields.

When the ARM purchases at higher discounts under market volatility, yields expand. The discount widening outpaces the queue lengthening, and the ARM captures the difference.

Market Volatility Leads to ARM Yield Spikes

On April 18th, 2026, attackers exploited a single-verifier vulnerability in KelpDAO's LayerZero bridge configuration, stealing approximately $290 million in rsETH. This cascaded into broader market volatility.

rsETH depegged approximately 15%. The panic spread beyond rsETH to the broader LST and LRT markets. Both stETH and eETH, assets with no direct exposure to the exploit, traded at widening discounts to their redemption values on secondary markets as holders rushed to exit and DEX liquidity thinned. At the same time, ARM yields spiked into the high double-digits.

That is the condition the ARM is built to capitalize on. By placing bids on redeemable assets during volatility, the ARM helps to stabilize secondary market pricing while earning yield for depositors.

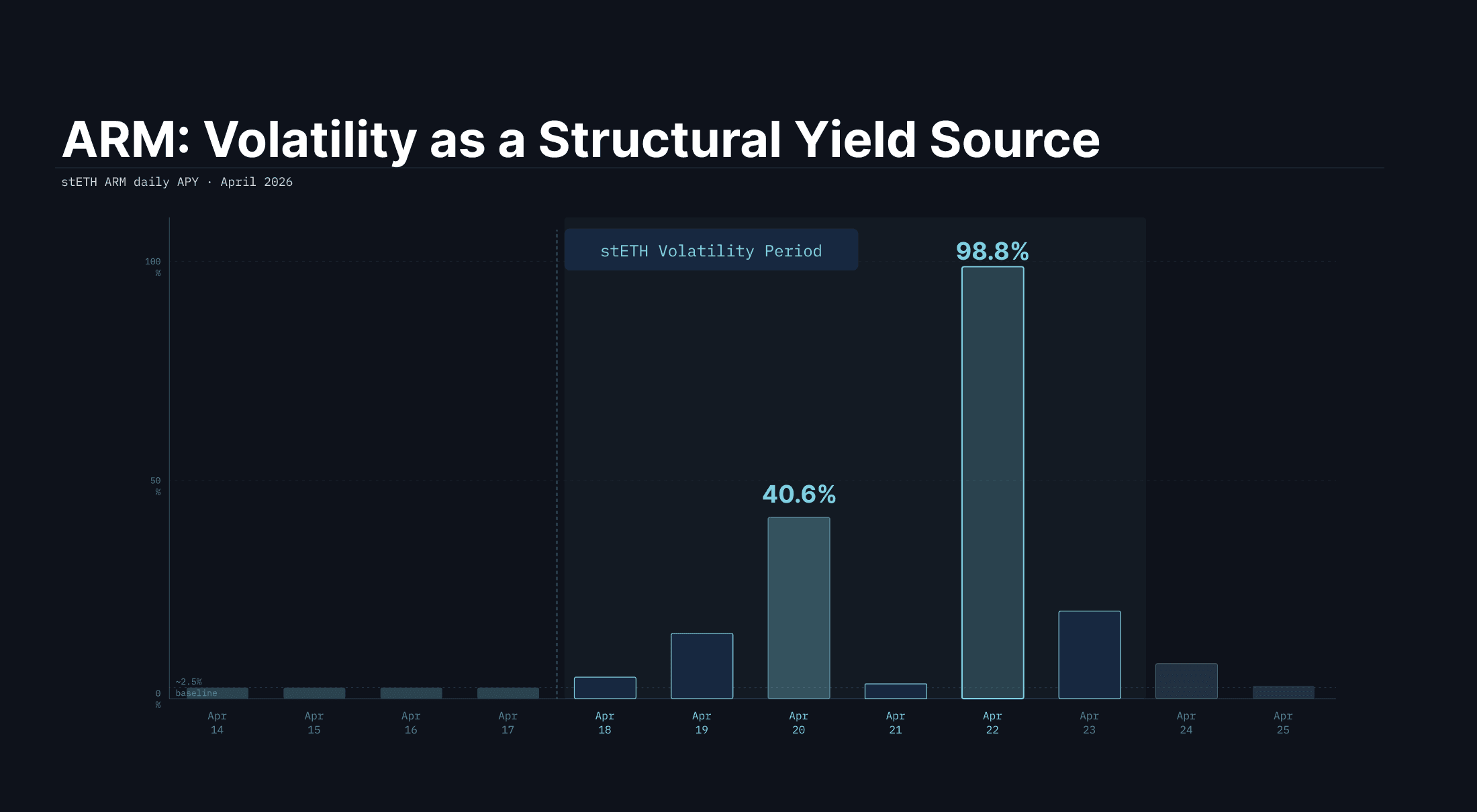

stETH ARM During Volatility: 98.8% APY on April 22nd

The stETH ARM entered the KelpDAO crisis week with approximately 4,000 ETH in TVL and a trailing 30-day APY of 2.5%. The baseline stETH staking yield over the same period was approximately 2.4%.

stETH's dislocation followed the broader market stress arc rather than the initial exploit shock. On April 20th, the stETH ARM generated a daily APY of 40.6% – roughly 17x the base stETH staking rate. By April 22nd, as the broader liquidity crisis deepened and DeFi TVL continued to contract, the stETH discount widened further.

The stETH ARM purchased stETH at a ~50 basis point discount on April 22nd, generating a daily APY of 98.8%.

eETH ARM Yield During Volatility: 47.8% APY on April 20th

The eETH ARM entered the same week with approximately 1,600 ETH in TVL. Its stress profile diverged from stETH's in a structurally meaningful way.

eETH is Ether.fi's liquid restaking token, built on EigenLayer. rsETH is also EigenLayer-based. When the exploit broke, the market's first reaction was to exit EigenLayer-adjacent exposure. eETH was caught in that initial wave.

The eETH ARM peaked first: 47.8% daily APY on April 20th, the same day the broader crisis was still unfolding. As the acute EigenLayer panic subsided over the following days, the daily APY fell: 26.6% on April 21st, and 20.4% on April 22nd.

ARM Vault Withdrawals During Stress Events

When the ARM is fully deployed in active redemptions, LP withdrawal requests queue behind the redemption cycle. Exits from the ARM become dependent on withdrawal request timing: capital must return from the redemption path before it can be claimable.

But the ARM enters stress events with capital already moving through the withdrawal queue. A direct stETH or eETH holder starts the redemption process when they decide to exit. The ARM may already have ETH returning from redemptions that were initiated before the LP asked to leave.

As of June 2026, the stETH ARM held 188.4 ETH in immediately available liquidity with 1,705.5 stETH already mid-queue, producing a median withdrawal time of approximately 13 minutes against Lido's native path of one to five days. 95% of stETH ARM withdrawal requests were processed within 18 hours.

The operational constraint of high utilization is real. It is a timing constraint, offset by increased returns to LPs. ARM Vault yield during stress events is determined by the spread at execution. Exit timing is determined by queue depth.

That is the ARM's position under stress: yield expands, exit timing is quicker than redeeming the underlying LSTs directly, and each purchase helps provide secondary market liquidity for token holders looking to exit.

Explore Origin’s ARM Vaults: app.originprotocol.com