Rethinking Redeemable Asset Liquidity

Most AMMs treat redeemable assets like standard correlated pools: stablecoin/stablecoin, RWA/stablecoin, or LST/ETH.

That works well enough when the job is routing swaps through deep liquidity. Curve, in particular, has been one of DeFi's most important venues for correlated assets.

But redeemable assets are different.

Their fair value is not anchored only by secondary-market liquidity. It is anchored by a redemption rail back into the underlying asset. That redemption rail creates an economic opportunity. And that is where ARM has a structural advantage.

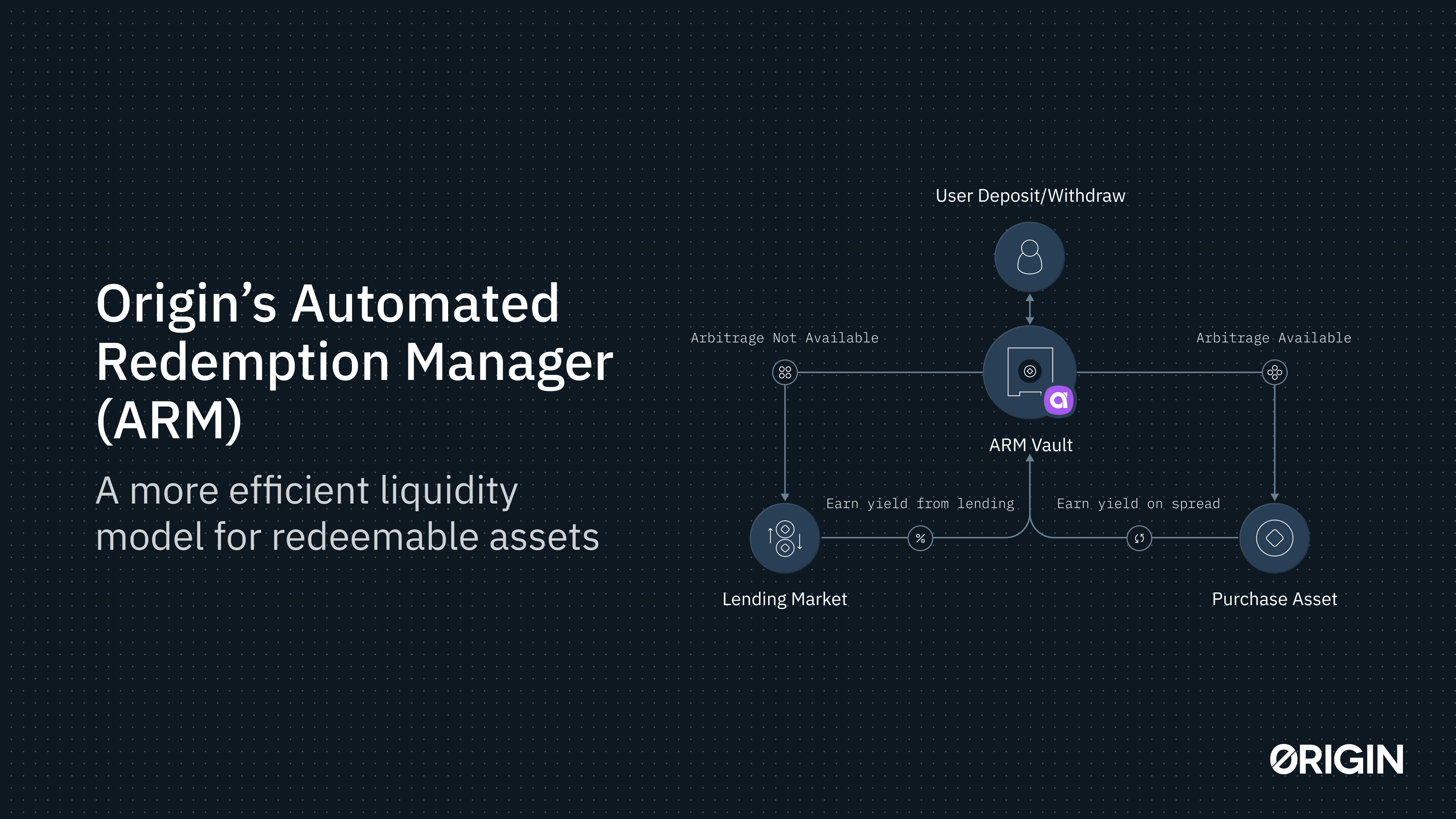

AMM LPs provide liquidity. ARM LPs monetize redemption.

Most AMMs are built to quote against pooled inventory. LPs deposit assets, traders route flow through the pool, and LPs earn swap fees and sometimes incentives for taking the other side of that flow.

ARM is different.

ARM is designed around assets with a redemption path. When a redeemable asset trades below redemption value, ARM can buy it at a discount, redeem it through the underlying protocol, and return the spread to LPs.

In other words, ARM turns the redemption queue into a source of LP yield. That is the core difference.

Common AMMs help the market trade around fair value. ARM helps pull price back toward redemption value while capturing the value of doing so.

Case study: stETH ARM vs Curve

Since stETH ARM LP deposits began on 17 October 2024, the stETH ARM has been materially more capital efficient than the major Curve stETH pools.

| Venue | Avg TVL (ETH) | Volume (ETH) | Volume / Avg TVL | LP earnings | Earnings / Avg TVL | Annualized |

| stETH ARM | 3,946 | 852,127 | 216.0x | 322.4 ETH | 8.17% | 4.95% |

| Curve stETH/ETH | 47,742 | 4,294,784 | 90.0x | 1,535.5 ETH | 3.22% | 1.97% |

| Curve stETH-ng | 13,182 | 979,741 | 74.3x | 468.0 ETH | 3.55% | 2.17% |

| Curve stETH-ng + max CRV | 13,182 | 979,741 | 74.3x | 524.4 ETH | 3.98% | 2.43% |

Curve has more total liquidity and more absolute volume. That is expected. But ARM does more with less.

The stETH ARM generated 216.0x volume over average TVL, compared with 90.0x for Curve stETH/ETH and 74.3x for Curve stETH-ng. The return profile is also stronger. stETH ARM LPs annualized at 4.95%, versus 2.79% for holding stETH over the same measurement window and 2.43% for Curve stETH-ng with max CRV.

That is the ARM thesis in one table: better LP returns from less capital.

Case study: eETH ARM vs Curve

The eETH ARM is newer and smaller, with LP deposits beginning on 30 October 2025. But the same structure appears. Again, Curve is larger in absolute terms.

| Venue | Avg TVL (ETH) | Volume (ETH) | Volume / Avg TVL | LP earnings | Earnings / Avg TVL | Annualized |

| eETH ARM | 218 | 52,533 | 241.2x | 5.4 ETH | 2.48% | 4.22% |

| Curve weETH/WETH-ng | 4,451 | 352,844 | 79.3x | 64.5 ETH | 1.45% | 2.46% |

| Curve weETH/WETH-ng + max CRV | 4,451 | 352,844 | 79.3x | 104.6 ETH | 2.35% | 4.01% |

| eETH ARM | 218 | 52,533 | 241.2x | 5.4 ETH | 2.48% | 4.22% |

But eETH ARM turns over far more volume per unit of liquidity: 241.2x average TVL, compared with 79.3x for Curve. And LP returns are higher: 4.22% annualized for eETH ARM versus 2.46% for holding Curve weETH/WETH-ng, and 4.01% for Curve with max CRV.

On a 7-day average basis, eETH ARM utilization was 595% versus 88% for Curve. Recent utilization is volatile, but the pattern is consistent: eETH ARM is much smaller, yet turns over materially more volume per unit of liquidity.

ARM keeps redemptions moving

A direct holder of stETH or eETH relies on the asset's native withdrawal path when they want ETH back. ARM works differently because it is already cycling inventory through that same redemption path.

When ARM buys a discounted redeemable asset, it can submit that asset for redemption and recycle the returned ETH back into the pool.

LP exits can therefore be served from two places: liquidity already available in the ARM, or ETH returning from redemptions that ARM had already started. That matters most when native withdrawal queues get long. A direct holder starts the clock when they decide to redeem. ARM may already have liquidity available, and it may already have assets moving through the queue.

The live analytics make the mechanism concrete:

| ARM | Native withdrawal path | ARM state on June 2, 2026 | ARM withdrawal history | Return comparison |

| stETH ARM | Lido withdrawals normally take 1 to 5 days. | 188.4 ETH available; 1,705.5 stETH already redeeming. | 10m minimum; roughly 13m median; roughly 18h p95 to become claimable. | 4.95% annualized versus 2.46% for stETH over the same window. |

| eETH ARM | EtherFi supports queued withdrawals and instant redemption when buffer liquidity is available. | 131.5 ETH available; 1,401.9 eETH already redeeming. | 10m minimum; roughly 13m median; roughly 27h p95 to become claimable. | 4.22% annualized versus 2.35% for eETH over the same window. |

The core point is not that ARM removes every redemption constraint or beats every native withdrawal in every state. It is that ARM keeps the redemption machinery running before an LP asks to exit, which can make exits faster than starting a native redemption from scratch.

Why ARM is purpose-built for redeemable assets

For redeemable assets, liquidity is not just about how much depth sits in a pool. It is about how the market prices the path back to the underlying asset.

When LSTs, LRTs, stablecoins, or RWAs trade below redemption value, someone can buy the discount, wait through the redemption process, and realize the spread. In a standard AMM, that spread is usually captured by whichever arbitrageur brings the pool back in line.

ARM is designed to route that same opportunity back to the LPs providing the liquidity.

That is the structural difference. AMMs are excellent at helping markets trade. ARM is built for the subset of markets where secondary-market liquidity can be connected directly to primary-market redemption.

For issuers, that can mean more capital-efficient liquidity. For LPs, it means yield can come from monetizing redemption mechanics rather than only from swap fees or incentives.

The data so far points in that direction: higher volume per unit of liquidity, stronger LP returns, and a liquidity model that turns redemption mechanics into an advantage rather than a constraint.

Explore Origin’s ARM Vaults on the Origin Dapp to become an LP.